Over the past 15 years, there have been reports of widespread embezzlement in the banking sector, involving the use of fake documents for land and apartment mortgages as collateral for loans. Sources said that despite selling mortgaged assets, most public and private banks have been unable to recover the defaulted loans.

In many cases, banks and buyers plotted to misappropriate large sums of money from these loans. Considering this situation, there is a need for an audit of loans taken with property as collateral. Stakeholders believe that criminal charges should be brought against those who embezzled funds to prevent further corruption in the financial sector. Additionally, there is a call for reforms in the banking sector.

According to a report published by Bangladesh Bank on Tuesday, defaulted loans have reached Tk 211,391 crore, accounting for 12.56 per cent of the total loans disbursed by banks. The total amount of loans now stands at Tk1,683,396 crore.

A study by the Bangladesh Institute of Bank Management (BIBM) in 2023 titled "Credit Operations of Banks" revealed that by the end of June last year, the total loans disbursed by banks against mortgaged land amounted to Tk 920,904 crore. Of these, 63.68 per cent were secured by real estate, including land, flats, and houses. Although such information has been reported in the media multiple times in the past, neither the government nor the central bank has taken any effective measures.

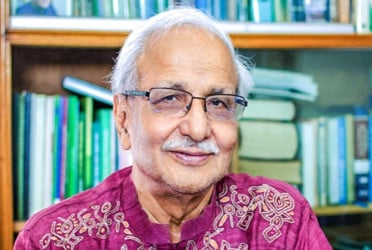

Contacted, Dr. Zaidi Sattar, Chairman of the private research institute Policy Research Institute (PRI), told Bangladesh Pratidin that fundamental reforms are needed to recover defaulted loans. There is no risk factor for large business owners, yet many of them are willful defaulters. This culture of willful defaulting needs to be eradicated.

He also said it is a big challenge to collect money from those who have taken loans with fake and same collateral to multiple banks and financial institutions. The new governor of Bangladesh Bank has undertaken initiative on these issues. Although the task is very difficult, it can be done.

Former President of the Federation of Bangladesh Chambers of Commerce and Industry (FBCCI), Md. Jasim Uddin, said, "Those who have looted bank funds using fake documents must be dealt with firmly. Legal action should be taken against both the involved customers and bank officials."

FBCCI Director Iqbal Hossain Chowdhury Jewel also demanded the highest punishment for bank looters on behalf of the business community, adding that the government must ensure exemplary punishment to prevent any unscrupulous individuals from embezzling public deposits in the future.

Industry experts said that the increase in irregularities, corruption, and embezzlement in the banking sector correlates with the rise in loans secured by mortgaged land. It is relatively easier to secure loans from banks by mortgaging land. There are allegations that banks have granted loans against state-owned land and disputed properties, with corrupt bank officials playing a role in these transactions. In most cases, the value of mortgaged land for influential individuals is significantly inflated, making it impossible to recover defaulted loans by selling the collateral.

According to the BIBM study, banks have managed to recover only 12.77 per cent of defaulted loans by selling mortgaged assets. This means that over 87 per cent of defaulted loans remain unrecovered despite the presence of collateral. The situation is even worse for loans written off by selling collateral. Despite the inability to recover loans by selling collateral, banks continue to increase loan distribution against mortgaged land. In 2010, the amount of loans disbursed against land mortgages was Tk141,834 crore, which was 47.94 per cent of the total loans distributed at that time.

The study further suggests that despite banks placing significant importance on collateral in loan distribution, they have not been successful in recovering defaulted loans by selling mortgaged assets. Only 12.77 per cent of defaulted loans could be recovered by selling collateral, while the recovery rate of defaulted loans through bank guarantees is 5.27 per cent.

Banks are writing off defaulted loans that have become uncollectible through normal processes. The recovery rate for written-off loans by selling collateral is only 10.43 per cent, and the recovery rate for loans written off against bank guarantees is only 3.27 per cent, said the study.

Bangladesh Bank's data shows that as of June of the last fiscal year, 63.68 per cent of customer collateral held against loans in the banking sector was immovable property. A decade ago, in 2010, this rate was 47.94 per cent. The trend of mortgaging land against loans has consistently increased over the past decade. The second-largest category of collateral in the banking sector is bank guarantees, accounting for 15.78 per cent. Other types of collateral include financial obligations (7.06 per cent), export documents and goods (5.12 per cent), machinery and fixed assets (1.37 per cent), and shares and securities (0.64 per cent).

Sources said that in many high-profile loan scandals in the country's banking sector, the value of mortgaged immovable property was found to be significantly overestimated. Despite the exposure of fraud by groups such as Hallmark, Crescent, and Bismillah Group, it was not possible to recover money by selling their mortgaged assets. Even after multiple auction notices, no buyers were found for the assets mortgaged by these scandal-linked groups. The situation is similar for the assets mortgaged by other groups that borrowed thousands of crores from the banking sector.

Sources also revealed that there have been numerous instances of large loans being taken from banks by mortgaging government-owned land in the capital, Dhaka, and adjacent areas. Similar cases have been reported across the country, including in Chittagong, where disputed and government land was mortgaged to obtain bank loans. Reports indicate that a significant portion of the land mortgaged to banks is disputed. Influential customers have mortgaged lands such as riverbanks, river erosion areas, land from reserved forests, hills, and land owned by various government institutions like railways to banks.

An influential politician of Awami League in Dhaka’s Mirpur had mortgaged illegally occupied land on the banks of the Buriganga and Turag rivers to National Bank in the private sector, securing a loan of nearly Tk 2,000 crore. With interest, this loan has now reached Tk 3,500 crore. The Bangladesh Inland Water Transport Authority (BIWTA) has conducted operations to reclaim the occupied land, but a large portion of the recovered land is still mortgaged to the bank.

In another case, a private bank accepted over an acre of land in Sahartok Mouza of Kapasia Upazila, Gazipur, as collateral. In return, a nominal housing company was given a loan of Tk 250 crore. The entire mortgaged property is land from the Brahmaputra River's erosion areas. There is a vast amount of government land in nearby areas like Keraniganj, Dohar, Demra, Savar, and adjacent districts. There is also a significant amount of Waqf State land in these areas. However, a large portion of these government and Waqf properties has been mortgaged to various banks by influential customers, against which banks have disbursed thousands of crores in loans. This raises concerns about how much of the bank loans disbursed against disputed land will be recovered.

bd-pratidin/GR