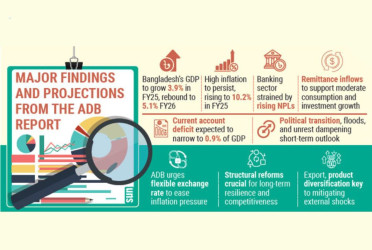

More than six months have passed since the Interim Government, led by Prof Muhammad Yunus, assumed power following the July Uprising, with the aim of dismantling autocracy and rebuilding Bangladesh. Significant reforms have been introduced across various sectors, including law, justice, parliament, the economy, and the banking system. However, despite these efforts, the Interim Government has struggled to regain investors' confidence amid ailing economic conditions marked by widespread corruption and mismanagement. Furthermore, the Bangladesh Energy Regulatory Commission (BERC) has initiated moves to raise gas prices, sparking a chaotic public hearing and deepening fears among investors.

The high price of the dollar and the ongoing dollar shortage have prevented the normal opening of Letters of Credit (LC). As the value of the taka continues to decline against the dollar, the cost of importing raw materials is steadily rising. Additionally, political uncertainty has led to worker dissatisfaction in many factories. Just yesterday, protests by workers erupted in industrial areas of Gazipur, Narsingdi, and Narayanganj, further increasing uncertainty and eroding trust among industrial entrepreneurs. Many investors are now grappling with the insecurity of their capital investments.

Industry leaders have said that the economy, which was already devastated by the COVID-19 pandemic, has yet to recover even after four years. Following the July Uprising, fascist Sheikh Hasina resigned and fled the country. Since then, chaos has prevailed across nearly all sectors. Many factories have closed due to the ongoing uncertainty, and numerous entrepreneurs have lost their capital and become bankrupt, leaving many workers unemployed. As a result, new investments are not coming in, and maintaining existing factories has become increasingly difficult, according to former President of BGMEA, Anwar Ul Alam Chowdhury Parvez.

if gas prices are raised amidst such uncertainty, shutting down factories might be the only option left, he said.

Kazi Sazedur Rahman, Managing Director of KPC Industries, told Bangladesh Pratidin, "the previous ousted government had destroyed the entire banking system and the economy. The current government has yet to take any effective initiatives to revive the economy. As a result, investors are unable to regain the confidence needed to move forward with investments."

Meanwhile, according to the Ministry of Finance and the Bangladesh Investment Development Authority (BIDA), there has been a significant decline in foreign investment.

In the first six months of the 2024-25 fiscal year (July-December), foreign investment has dropped to nearly one-fourth of the amount from the same period last year. During this period, foreign investment fell by more than 71% compared to the previous year. The Ministry of Finance states that institutional weaknesses are evident in making business and trade easier. Additionally, ongoing political uncertainty in the country is also preventing new investments. At the same time, the revenue collection situation is not favorable.

Former President of the Dhaka Chamber of Commerce, Abul Kasem Khan, said, "ensuring capital security is crucial for boosting investment and employment. Along with this, securing a conducive investment environment and maintaining political stability are necessary, and none of these factors are currently present in Bangladesh. These issues have been ongoing for a long time. As a result, industrial entrepreneurs are not making new investments."

Translated by ARK/Bd-Pratidin English